.png)

Over the past two weeks, I've had many calls with Israeli investors and tech leaders, all asking the same question: what does the industrial market actually look like?

It makes sense that they're asking.

The reshoring wave is accelerating. A generation of engineers is retiring faster than they can be replaced. And the cost of industrial hardware has collapsed so dramatically that the physical layer is no longer where companies win. Three forces converging at the same moment, and the Israeli tech ecosystem is beginning to (re)notice.

I kept finding myself giving the same recap, so I decided to write it down.

What makes this particularly interesting from an Israeli perspective is that this country has been quietly building the intelligence layer for the world's largest industrial companies for decades. Industrial is not a new topic here. The world's leading chip inspection platform. The backbone of Siemens' factory software. The data infrastructure that runs semiconductor and automotive production lines globally. All built by Israeli teams. Most people in Israeli tech don't know this story, because the companies that told it got acquired quietly, absorbed into giants like KLA, Siemens, and Emerson, and just focused on working.

This is the next chapter.

The origin story most people skip

Israel is known today for cybersecurity. Check Point, CyberArk, SentinelOne, Wiz, a lineage of security companies so dominant that roughly one in three global cybersecurity unicorns traces roots to Israeli founders. It's the story everyone tells.

But there's an older story, and it runs deeper.

In the early 1960s, a cluster of companies emerged that would define what Israel could build. ECI Telecom, founded in 1961, built the switching and transmission equipment that connected telephone networks across the developing world; it was Israel's first serious industrial exporter. Tadiran, founded in 1962, became Israel's largest electronics manufacturer, supplying military communications systems, consumer electronics, and industrial batteries to customers across four continents.

And in that same year, Uzia Galil, an electrical engineering graduate of the Technion, founded Elron Electronic Industries in a rented flat in Haifa. Regarded by many as the "Fairchild of Israel," Elron was founded with just $160,000 and generated $1 million in annual revenue within three years.

Galil's bet was explicit: that knowledge-based industrial companies, not natural resources or cheap labor, were the path to economic sovereignty for a young nation with neither.

His conviction paid off in ways few could have anticipated.

In 1967, after France embargoed key arms sales to Israel (they had been providing nearly 80% of Israel's arms by 1966), Elron was ready to help fill the gap. Elbit, a spin-off of Elron, built one of Israel's earliest microcomputers. Elscint, another spin-off producing medical imaging devices, became the first Israeli firm traded on Wall Street in 1972. "Hundreds of companies grew from people who left Elron," Galil once said.

In parallel, Motorola opened its first overseas R&D center in Israel in 1964, initially to develop wireless products. Intel, Microsoft, and Apple built their first overseas research and development centers in Israel, and other high-tech multi-national corporations, such as IBM, Cisco Systems, and Motorola, have opened facilities in the country. Intel developed its dual-core Core Duo processor at its Israel Development Center in Haifa.

Then came the invention that put Israeli manufacturing on the global map: In 1989, Dov Moran (whom many founders know from his fund, Grove Ventures), a graduate of the Technion who had served in the Israeli Navy commanding its advanced microprocessor department, formed M-Systems, a pioneer in the flash data storage market. The company invented the USB flash drive (DiskOnKey), the FlashDisk (DiskOnChip), as well as several other innovative flash data storage devices. In 2006, M-Systems was acquired by SanDisk for $1.6 billion, cementing the USB flash drive as a global standard.

In the early 1980s, Control Data Corporation, a partner (and eventual shareholder) in Elron Electronic Industries, formed the country's first venture capital firm (Athena Venture Partners, founded in 1985). The roots of Israeli venture capital are in industrial technology, in the conviction that building things with engineered intelligence was a legitimate, fundable path. That conviction never went away. It just got overshadowed for a decade by the cybersecurity boom.

While the world was watching Check Point and CyberArk, Israeli industrial software teams were quietly providing the operating system for the world's largest manufacturers with exits worth billions to Siemens, KLA, NI/Emerson, and SKF. The exits didn't stop.

And now the next generation is building.

Three patterns that define the ecosystem

After mapping 30 companies across five categories, three structural observations emerge.

1. Tacit Knowledge is the New Oil:

The "Silver Tsunami", a generation of retiring engineers, technicians, and procurement specialists, is the defining macro force behind this entire map. The knowledge required to scope a complex automation project, program a PLC, diagnose a field failure, or manage a defense-grade supply chain has never been written down. It lives in people. And those people are leaving.

Companies are building institutional memory infrastructure, a fundamentally different category from productivity tools. When the last person who knows how to configure that motion controller retires, the knowledge walks out the door with them. These companies exist to prevent that. Galil understood this in 1962: knowledge-based industry requires mechanisms to transfer knowledge. Those mechanisms are finally being built at AI scale.

2. Anti-Legacy Positioning is Universal:

Every company on this map succeeds by bypassing the slow, cumbersome systems of the past, acting either as an intelligent overlay on top of existing infrastructure, or as a lightweight AI-native replacement that deploys in weeks rather than the months a legacy system would require. The Anti-MES. The Smart PIM. The AI layer on top of the PLC. The AI Application Engineer. The replacement for email-and-PDF procurement. The CAM layer that existing tools don't have.

This is partly a go-to-market reality: attacking legacy is an easier narrative than greenfield creation, but it's also a genuine technology claim. The tools built for industrial operations over the past 30 years were not designed for AI. Bolting AI onto them doesn't work. The industrial software stack is being rebuilt from scratch, and Israeli teams have an incredible opportunity to build a meaningful portion of it.

3. Hardware Commoditized. Intelligence is the New Moat:

The first generation built the physical layer. Elron, Tadiran, ECI they made things: telecommunications equipment, defense electronics, industrial sensors. The competitive advantage was in the hardware itself.

The second generation built software on top of that hardware. Orbotech's inspection machines ran on proprietary vision software. Valor automated the handoff between design and factory floor. Presenso connected bearings to the cloud. The software was valuable, but it was still tethered to physical assets you needed the machine to run the intelligence.

This generation builds intelligence. Software that has no physical dependency. The robot brand doesn't matter. The PLC vendor doesn't matter. The ERP system doesn't matter. Every company on this map sells AI that works on top of whatever infrastructure the customer already has, and that's a direct consequence of hardware commoditization. When a cobot that cost $100,000 in 2015 costs $15,000 today, the physical layer stops being the moat. The intelligence layer becomes everything.

And intelligence compounds in ways that hardware never could. Every new customer makes the model smarter. Every additional data point sharpens the product. The Israeli industrial companies of the 1960s competed on manufacturing capability. The companies of the 1990s competed on software specificity. The companies on this map compete on accumulated intelligence, and that is the most defensible position any of the three generations has ever occupied.

What ultimately unites all companies on this map is a single shared thesis:

Industrial operations are dense with knowledge work that has traditionally masqueraded as manual labor. From writing PLC code to scoping a complex RFQ, from reviewing an engineering drawing to diagnosing a machine failure in the field, these tasks require expertise and attention, both of which can now be systematized at scale. The systematic capture and deployment of hard-won industrial expertise, at the moment it's needed, by the person who needs it. That is what Israeli industrial startup teams are building.

The landscape in 2026

A note on methodology

This map covers companies founded in the last decade, since 2015 (with a legacy section for older companies actively shipping AI and notable exits), headquartered or founded in Israel or by Israelis, building software-first AI products for the industrial sector. We excluded pure hardware or raw-material (ex: new chemicals) plays. Cyber for industrial. Defense-only, semiconductor-only, and construction-tech-only companies. Companies where industrial is a secondary market. A handful of judgment calls were made on companies with dual US/Israel presence; in those cases we included companies where a majority of the founding team is Israeli and meaningful product development happens in Israel.

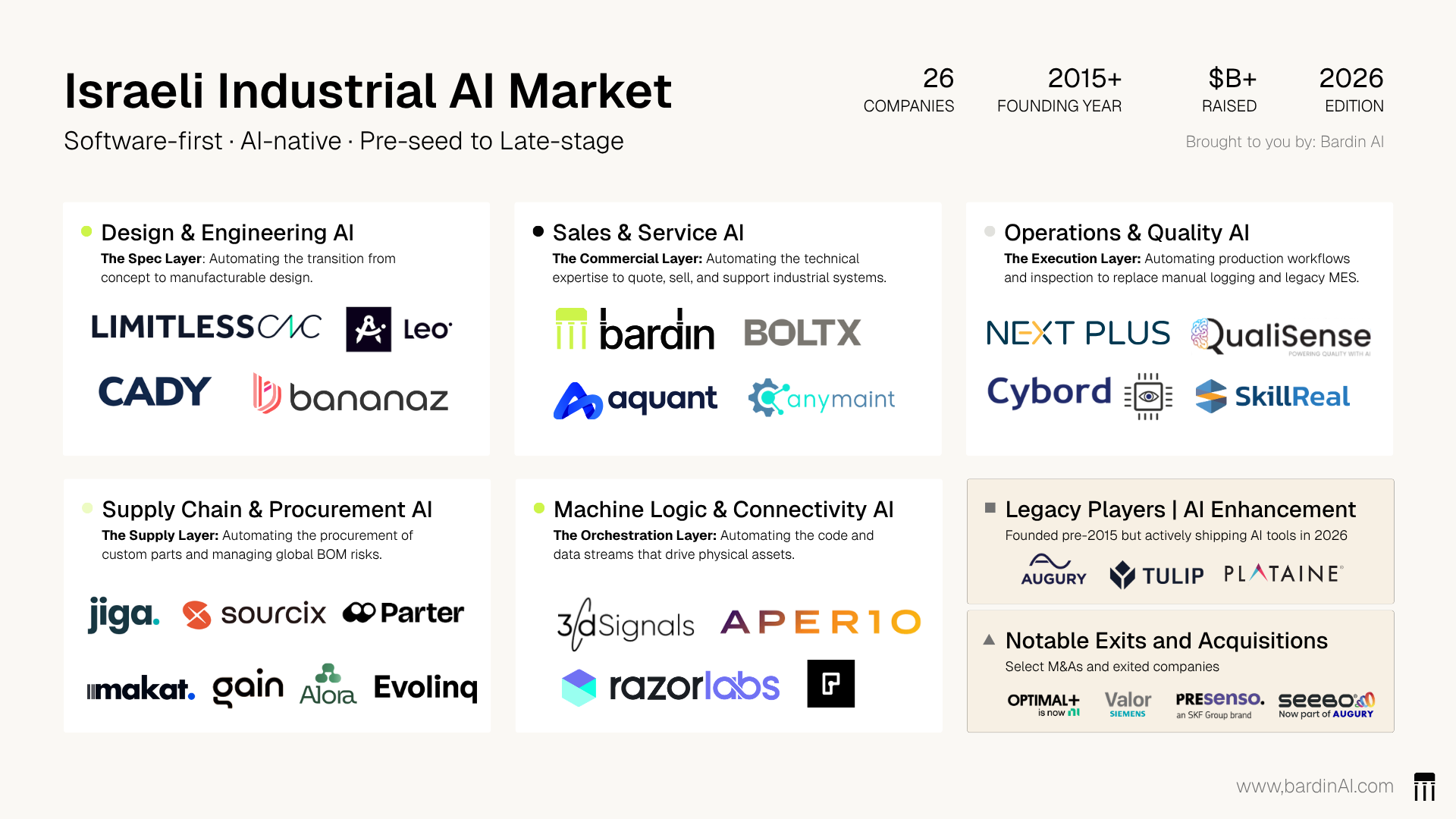

The five categories were drawn by two dimensions: who buys it, and where in the industrial process it sits. Each layer represents a distinct moment in the lifecycle of an industrial product, from concept to customer to machine, and a distinct person responsible for that moment:

- The Spec Layer: before anything is built. The mechanical or electrical engineer turning a concept into something manufacturable.

- The Commercial Layer: before and after the sale. The applications engineer, sales engineer, and service team getting the product to the customer and keeping it running.

- The Execution Layer: on the production floor. The plant manager and quality engineer responsible for what happens once manufacturing begins.

- The Supply Layer: upstream of production. The procurement manager and sourcing engineer making sure the right parts arrive at the right time.

- The Orchestration Layer: underneath everything. The automation and controls engineer responsible for the machines, logic, and data streams the entire operation depends on.

Five moments in the process. Five buyers. One stack.

This is a living report. If you know of a company that belongs on this map, reach out.

Engineering & Design AI

The Spec Layer: Automating the transition from concept to manufacturable design.

Companies: Leo AI, Bananaz, LimitlessCNC, CADY Solutions

Users: Mechanical and electrical engineers, R&D teams, CAD users

Buyer: Head/VP of Engineering, R&D

What unites these four companies is a shared thesis: the pre-product engineering phase is dense with knowledge work that masquerades as manual labor. Comparing drawings. Writing toolpaths. Checking schematics. Searching for components. These tasks require expertise and attention, both of which can be systematized at scale.

LimitlessCNC (founded 2024, $4.1M Seed) attacks a different bottleneck: the step between CAD file and machined part. CNC programming, writing the toolpaths that tell a machine how to cut, is a specialized skill that takes years to develop and is increasingly concentrated in a shrinking pool of aging machinists. LimitlessCNC's physics-based AI agents reduce programming time by up to 80%.

Bananaz (founded 2023, $5.3M Seed) sits one step later in the engineering lifecycle, automating the review and comparison of engineering drawings, the kind of manual, error-prone work that consumes a significant portion of an engineer's time and is responsible for a meaningful share of production defects. When a product changes, someone has to compare the old drawing to the new one, identify every difference, and update the engineering change order. Bananaz does this with computer vision and AI.

Leo AI (founded 2023, $9.7M Seed) is building what it calls a Large Mechanical Model, a proprietary AI trained exclusively on machine parts, engineering documents, and design patterns. It can generate CAD assemblies, answer design questions in context, and surface relevant components from a company's PDM.

CADY Solutions (founded 2020, $8.9M raised) tackles a different failure mode entirely: the electrical schematic. PCB designs that look correct but contain subtle errors that only surface after expensive fabrication. CADY uses NLP and computer vision to read component datasheets and cross-check them against circuit designs, catching errors before production.

Sales & Service AI

The Commercial Layer: Automating the technical expertise to quote, sell, and support industrial systems.

Companies: Bardin AI, BoltX, Aquant, AnyMaint

User: Applications engineers, sales engineers, field service and maintenance teams

Buyer: Head/VP of Sales, Applications, Revenue, Service

Walk into almost any industrial company (an OEM, a systems integrator, a distributor) and you will find the same problem in a slightly different form. There is a person, sometimes two, sometimes three, who holds a disproportionate amount of institutional knowledge. The applications engineer who knows which product configuration works in which environment. The senior technician who can diagnose a machine failure in minutes. The veteran rep who can scope a complex solution on the first customer call. These people are valuable beyond measure. They are also, almost universally, either close to retirement or stretched across more demand than one person can serve. The companies in this category are building AI that captures, encodes, and deploys that expertise, so it can be accessed by anyone on the team, not just the person who has been there for 25 years.

Bardin AI (founded 2024, pre-seed) is building application knowledge infrastructure for industrial automation OEMs, distributors, and systems integrators. The core insight is that the knowledge required to scope, sell, and support complex industrial automation solutions (a mobile robot deployment in an automotive plant, a conveyor system for a pharmaceutical facility, a vision-guided assembly line for electronics manufacturing) is largely tacit, and lives in experienced people, not in documentation or software systems. Bardin captures that knowledge and makes it available to every applications engineer, every salesperson, and every integrator partner.

BoltX (founded 2023, Seed) addresses the same knowledge gap in maintenance. Their physical AI copilot is designed so that any technician, even one who has never been trained on that specific machine, can diagnose and fix complex industrial equipment. The company's positioning is explicitly tied to the skilled-labor crisis: as experienced maintenance technicians retire, the knowledge that makes complex machines operable is disappearing with them.

Aquant (founded 2015, $69M raised) has been working on this problem the longest of the four. Their service intelligence platform helps industrial field service organizations improve first-call resolution rates, reduce escalations, and capture institutional knowledge systematically across service teams. They've reached Series C scale doing it. (founded 2021, ~$600K raised) rounds out the category with a complementary angle: maintenance workflow management itself.

AnyMaint provides the CMMS and EAM layer, the system of record for work orders, preventive maintenance schedules, parts inventory, and maintenance history. Built with a simplicity-first philosophy specifically for frontline technicians in industrial plants, it integrates with WhatsApp because that's what workers on a factory floor actually use.

Operations & Quality AI

The Execution Layer: Automating production workflows and inspection to replace manual logging and legacy MES.

Companies: Next Plus, SkillReal, Cybord, QualiSenseUser: Plant managers, ops teams, quality engineers

Buyer: VP or Head of Manufacturing and/or Operations

The most established category on the map in terms of problem definition. Plant managers have been buying MES software for 30 years. The Israeli companies in this space are attacking the same buyer with a fundamentally different value proposition: lighter, faster, AI-native, deployable in weeks rather than months.Next Plus (founded 2015, Series A) automates production and compliance workflows as the "AI-first Anti-MES," a deliberate counter-positioning against heavyweight Siemens, SAP, and Oracle systems. Their platform covers production, maintenance, quality, and compliance in one integrated system, SOC 2 and FDA 21 CFR Part 11 compliant, built to be deployed by operators rather than IT teams.SkillReal (founded 2020, Series A) is digital twin technology that automates precision in-line manufacturing inspection, building digital representations of production lines that enable real-time quality intelligence without disrupting physical workflows.Cybord (founded 2018, $12.7M) deploys visual AI that automates electronic component inspection at the SMT line, detecting counterfeit, defective, or tampered components before they get soldered to a board, with a database of over 4 billion components and an air-gapped version launched in 2025 for defense and aerospace.QualiSense (founded 2021, $8.5M) is an AI system that automates finished-product quality audits, with autonomous inspection across production lines that reduces manual inspection time and increases defect detection accuracy.

Supply Chain & Sourcing AI

The Supply Layer: Automating the procurement of custom parts and managing global BOM risks.

Companies: Jiga, SOURCIX, Makat, Gain, Parter, Evolinq, AloraUsers: Procurement managers, sourcing engineers, hardware teams

Buyer: VP/Head of Procurement and/or Supply Chain

The density of Israeli supply chain AI companies traces directly to the country's manufacturing DNA. Companies supplying Elbit, Rafael, and IAI operate with zero tolerance for component shortages, where a single missing part can halt a production line building systems worth millions. Generations of engineers and procurement professionals trained in that environment become founders who build for the problems they know viscerally. The process of procurement in hardware manufacturing has resisted digitization for decades because it is deeply human, document-heavy, and relationship-intensive. AI finally enables the right tools to automate it.Jiga (founded 2020, $19M Series A) is the most mature and best-known. It's a marketplace and platform where engineers upload drawings and get matched to vetted manufacturers, compressing custom parts procurement from weeks to hours. Its customers include NASA, Siemens, Tesla, and Apple.SOURCIX (founded 2024, Seed) and Makat (founded 2022, $3.5M) are more focused variants. SOURCIX handles project-level procurement for custom mechanical parts, building institutional memory into the sourcing process so that every RFQ benefits from prior decisions. Makat is narrower still, an AI purchasing agent specifically for electronic components, providing real-time stock availability and pricing for OEMs and contract manufacturers.Gain (founded 2024, $12M Seed) is building AI employees for procurement: autonomous agents that handle the long tail of purchasing that consumes so much human attention but adds little strategic value.

Parter (founded 2023, $5.5M Seed) is the most comprehensive of the group, a hardware intelligence platform that unifies BOM management, component lifecycle tracking, tariff intelligence, risk monitoring, and sourcing automation across engineering, supply chain, and R&D simultaneously.Evolinq (founded 2023, pre-seed) deploys autonomous AI agents that read supplier emails in any format, extract confirmations and exceptions, and sync them into ERP systems automatically.Alora (founded 2024, pre-seed) monitors supply chain risk at the BOM level in real time, connecting component-level signals (EOL notices, price spikes, shortage alerts) directly to their impact on specific builds and delivery commitments.

Machine Logic & Connectivity AI

The Orchestration Layer: Automating the code and data streams that drive physical assets.Companies: PLCs.ai, 3DSignals, Razor Labs, Aperio

User: Automation engineers, controls engineers, plant & asset managers

Buyer: VP/Head of Manufacturing and/or Machining

Every industrial operation runs on machines, and those machines run on logic, data, and connectivity. This category covers the companies building AI for the physical control and data layer: automating the programming of machine logic, the tracking of machine health, the prediction of machine failure, and the validation of the data that all other AI depends on.3DSignals (founded 2015, $26.6M) automates machine health and utilization tracking via non-invasive acoustic sensors, with no PLC integration and no production disruption. Most factory machines generate no usable data. 3DSignals changes that in hours.

PLCs.ai (founded 2024, $4M Seed) automates the generation and troubleshooting of PLC code, the programs that control every automated machine in a factory. PLC programming is a specialized discipline with a shrinking talent pool. PLCs.ai's industrial-specialized AI agents read and understand existing PLC code, then enable engineers to update, debug, and generate new logic in natural language.

Razor Labs (founded 2016, the first AI company listed on the Tel Aviv Stock Exchange) automates predictive maintenance for heavy industrial assets via its DataMind AI platform. Deep learning sensor fusion predicts critical failures weeks in advance. Customers span mining, manufacturing, and utilities globally.Aperio (founded 2016, $8.5M raised) automates the validation and integrity of industrial sensor data in real time. Unsupervised ML learns each sensor's unique fingerprint and detects anomalies, malfunctions, or deliberate data manipulation, solving the garbage-in-garbage-out problem that undermines every other industrial AI platform built on top of it.

The established players: roots and reinvention

Three companies predate the 2015 cutoff used for the main map, but earn a separate mention precisely because they demonstrate that Israeli industrial AI isn't just a 2026 phenomenon.Augury (founded 2011, $375M+ raised, unicorn) pioneered AI-based machine health monitoring and predictive maintenance. It spent 2025 aggressively scaling its platform with new AI capabilities, raising $75M at a $1B+ valuation.Tulip (founded 2014 by Israelis Natan Linder and Rony Kubat, $273M raised, $1.3B valuation) recently reached a new milestone on a Series D led by Mitsubishi Electric, acquired Israeli startup Akooda, and opened a dedicated R&D hub in Tel Aviv, a homecoming of sorts.Plataine (founded 1997 in Petah Tikva, the same industrial heartland that hosted some of Israel's earliest electronics manufacturers) is the elder statesman. Its production scheduling and material traceability platform is used by Airbus, IAI, Triumph, and the broader aerospace and defense supply chain. In early 2025, it launched a full AI Agents suite. A company that predates the startup nation era, still shipping meaningful technology.

Israeli companies solve hard problems

The companies on this map are the latest generation of a pattern that has been repeating for decades: Israeli industrial software teams solve hard problems, get acquired by the world's largest industrial companies, and become the invisible backbone of global manufacturing.

The exits tell the story more clearly than any narrative can.

The Spec Layer has an exit: Valor Computerized Systems, acquired by Mentor Graphics (now Siemens) in 2010, built the Design-for-Manufacturing software that is now the backbone of Siemens' industrial software suite. If you use Siemens software in a factory today, you are almost certainly running technology built by an Israeli team. Leo AI, Bananaz, and LimitlessCNC are building the next generation of that same layer.

The Execution Layer has multiple exits: Orbotech, acquired by KLA for $3.4 billion in 2019, was the world leader in using AI and computer vision to find defects in PCBs and flat panel displays. It remains the largest exit in the history of Israeli industrial technology and established Israeli vision intelligence as the global gold standard for electronics manufacturing. Optimal Plus, acquired by NI (now part of Emerson) for $365 million in 2020, built the pure-play big data analytics platform that analyzes production data for semiconductors and automotive electronics to predict quality failures. Vanti, acquired by Marvell in 2024, automated manufacturing quality SaaS, bought by a global chip giant to automate their own internal production intelligence. Inspekto, acquired by Siemens in 2023, built autonomous machine vision that lets non-experts deploy high-end visual inspection. Seebo, acquired by Augury in 2022, built the AI process health layer for chemical and food industries, a rare industrial-to-industrial merger that helped create the first Israeli-founded industrial software unicorn. QualiSense, Cybord, and SkillReal are building the next generation of this layer.

The Orchestration Layer has an exit: Presenso, acquired by SKF in 2019, built the first truly cloud-native automated machine learning platform for predictive maintenance. SKF, the world's largest bearing company, bought them specifically to turn their physical bearings into digital services. PLCs.ai, 3DSignals, Razor Labs, and Aperio are building the next generation of this layer.

The Commercial Layer has an exit too: Fieldbit, acquired in 2021, built the first AR/AI platform for industrial field service knowledge transfer, the predecessor of what Bardin, BoltX, and Aquant are building today. The Commercial Layer is now producing companies worth watching, and it is structural: previous generations of AI couldn't encode the nuance of industrial expertise. "This motor works in this application but not that one." That kind of contextual, combinatorial knowledge resisted every software paradigm until accessible AI models arrived. The technology readiness and the market need finally converged at the same moment.

The exit logic is also becoming clear. PTC owns the engineering layer. SAP owns the supply chain layer. Siemens owns the execution layer. None of them own the commercial layer, the software that helps industrial companies actually sell and support the products built on top of all that infrastructure. That gap is enormous, measurable in revenue terms, and it's the one layer where the ROI of AI is most directly attributable. The previous wave of exits proved the infrastructure layers had value. The next wave will come from whoever owns the revenue layer, and that race is just beginning.

The world's largest industrial incumbents, companies with decades of engineering resources and billions in R&D, went to Israel to buy the intelligence layer they couldn't build themselves. Every category on this map has a multi-hundred-million-dollar exit behind it.

The 26 pre-exit companies here are the next cohort in that same pattern, building the intelligence layers that the next generation of industrial giants will need, and almost certainly acquire.

Which brings me back to those investor calls.

That question has a longer answer than any single conversation can hold. But the short version is that the founders building in this space carry the right background, the right obsessions, and arrived at exactly the right moment. The macro forces making industrial AI inevitable, the retirements, the reshoring, the hardware commoditization, are present realities, and they are accelerating.

Israel has been here before. It built the physical layer, then the software layer, and now it's building the intelligence layer. Each generation went deeper, and each generation produced exits that reshaped global industrial technology.

We are proud to be part of the third generation of Israeli industrial companies. And we are just getting started.

About Bardin AI

Bardin AI builds application knowledge infrastructure for industrial automation OEMs, distributors, and systems integrators. Industrial companies run on expert knowledge, the applications engineer who knows which product works in which environment, the senior rep who can scope a complex solution on the first call, the channel partner who needs to sell confidently without calling headquarters. Bardin captures that knowledge and deploys it across every sales and service touchpoint, so the expertise of your best people scales across your entire commerical and customer-facing team.

www.bardinAI.com

.png)